The price/sf exceeds what the Expedia Tower got, by quite a bit. It appears the market for leased up, Class A property in CBDs continues to strengthen buoyed by deep pocketed investors looking to take advantage of depressed market conditions. Of course, the coup of the decade still belongs to Northwest Mutual's steal of the WAMU Center last year. The lessons of WAMU Center are that it pays to look for a motivated Seller with a low cost basis (JP Morgan got it almost free as part of the Washington Mutual rescue, and, didn't want it) and have tenants waiting in the wings to move in (Northwest Mutual is the parent of Russell Investments who is moving into the tower).

Rents are down over 20% (and going lower).

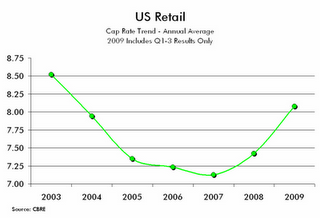

Rents are down over 20% (and going lower). Vacancies are up nearly 13% (and going higher). Capitalization rates are probably 300 bps higher (and as the meltdown continues, headed higher). Today our hypothetical building has probably lost over 50% of its value:

Vacancies are up nearly 13% (and going higher). Capitalization rates are probably 300 bps higher (and as the meltdown continues, headed higher). Today our hypothetical building has probably lost over 50% of its value:

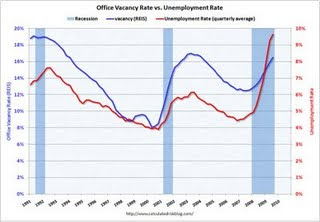

Nationwide Office vacancy rates are over 16%, after bottoming at 8%. Office vacancies appear to lag unemployment pretty closely. A top in unemployment will be a good confirmation of a coming low in office vacancies. The sharp increase in unemployment ensures that current leaseholders have ample room to house new employees prior to needing additional space, diminishing demand for office space.

Nationwide Office vacancy rates are over 16%, after bottoming at 8%. Office vacancies appear to lag unemployment pretty closely. A top in unemployment will be a good confirmation of a coming low in office vacancies. The sharp increase in unemployment ensures that current leaseholders have ample room to house new employees prior to needing additional space, diminishing demand for office space.