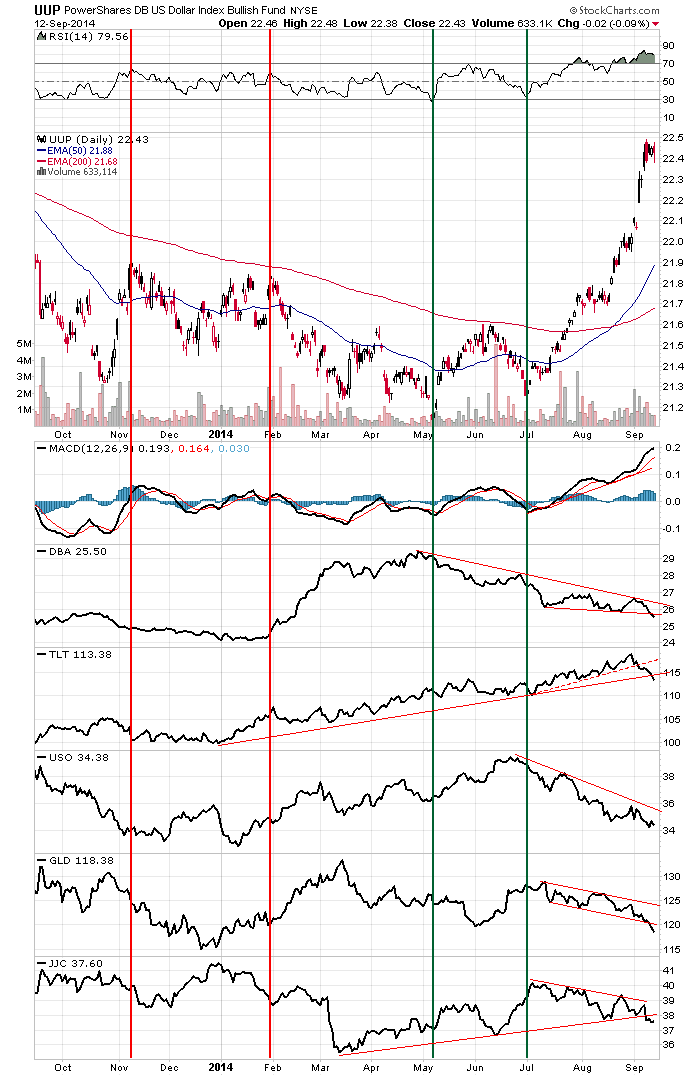

Last month's comments out of the ECB regarding the potential for some form of QE launched the US Dollar out of a 12 month trading range.

The strength of the move is undeniable, but the indicators are clearly into Overbought territory. The strong dollar has been weighing on Commodities.

Early this year, Commodities broke out off a 3 year wedge. DBA is currently backtesting the breakout as the Indy's have reset. A move up the ma's would represent a new breakout with a first target of 29.

The Daily chart shows the top of the wedge. It also reveals a smaller wedge that has formed since the US Dollars July low. The smaller wedge was broken last week. The Indy's look like the have room, but there needs to be a break of 26.85 for the big move.

Corn looks interesting. After getting whacked for 15% in May-June due to bumper crop reports, it got taken for another 15% after the US Dollars low. Since then Corn has been wallowing between 25 & 26 on somewhat surprising volume. It seems that the Indicators need more time to reset but Corn looks attractive above 26.5 with an obvious stop at 25.25. With the first target of 30 a return of 10% would make a punt worth it.

Other non-agricultural commodities are showing potential bottoms including Oil, Copper & Unleaded Gas. All ears will be on the ECB this Thursday when they announce their monetary plans. If they announce QE plans, the size & scope will determine the markets moves. Some QE is already priced into the US Dollar. No QE, or, smaller than expected might provide the fuel for the commodities markets to make a comeback.